A previous article on this site discussed depreciation and related topics. It went into detail about straight-line depreciation, MACRS depreciation, various calculations/resources and related topics like recapture.

This post will serve as a guide to the MACRS depreciation method, which is more complex than straight line. MACRS depreciation allows businesses to take larger deductions in earlier years that decrease overtime for assets like real property, vehicles, software, and office equipment. Each asset class has its own unique rules that must be adhered to in order to stay tax compliant.

For example, businesses that own rental property that was put in place after 1986 MUST use the MACRS method. Also, there are many factors like business use percentages and Section 179 that influence this deduction. This guide will also mention how MACRS applies to a variety of assets, especially solar panels.

How to calculate the MACRS depreciation method

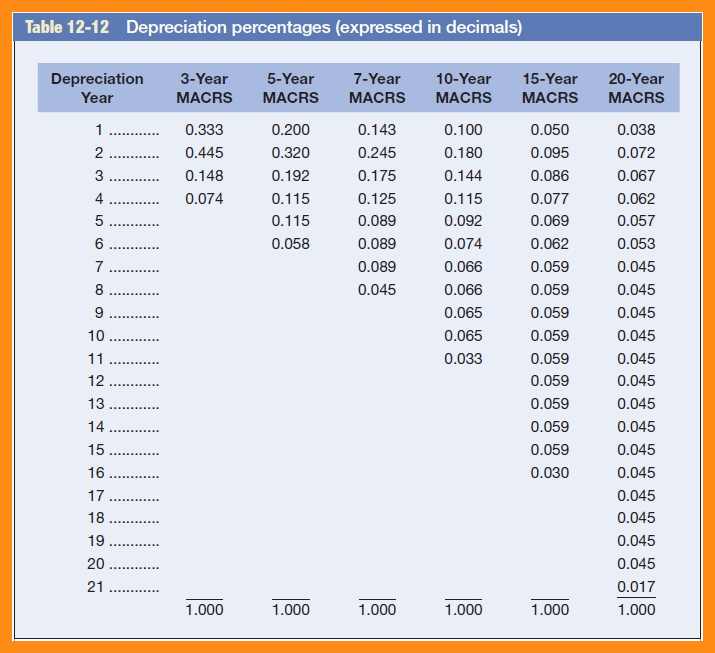

The MACRS depreciation method is more complex than straight line as it’s impacted by more factors. However, the simple MACRS formula is cost basis of the assets x depreciation rate. So, machinery equipment with a cost basis of $10,000 and a depreciation rate of 5% would have a $500 MACRS deduction. Also, it’s wise to refer to IRS pub 946, which has detailed tables on depreciation rates, percentage table, and methods.

There are four main ways to calculate depreciation which are GDS using 200% DB, GDS using 150% DB, GS using SL, and ABS using SL. These can be easily understood by breaking down each type below:

GDS 200% DB

This stands for general depreciation and declining balance, which is essential for calculating MACRS. This way enables businesses to take larger deductions in the earlier years, which decline over time.GDS is the more general of the two systems and is used more frequently than ABS. This standard is used for non-farm equipment that have recovery periods of 3,5,7, and 10 years.

Recovery periods are also known as useful lives and are the time periods the asset is expected to last before obsoletion. The 200% reflects the double percentage used to calculate depreciation and can be calculated by twice the straight line rate x asset’s cost basis.

GDS 150% DB

This standard is nearly identical to the above GDB 200%. It also allows businesses to take higher deductions in earlier years and applies to the same assets as GDB 200% However, it also includes farm property and 15 to 20-year property (excluding real property). The 150% refers to the calculation which is 50% higher than the straight line rate.

GDS using SL

This method uses the straight-line depreciation (SL) which allows equal annual depreciation deductions for nonresidential and residential property. It also applies to section 168k property. Section 168k refers to new bonus depreciation rules which enable businesses to take additional depreciation deductions on new assets placed in service.

ABS using SL

ADS stands for alternative depreciation system and is similar to the GDS/SL method. It uses the straight-line method, but it applies to international real property and tax-exempt property. ABS can be used for property that has less than 50% business use. This standard uses the SL method, which has equal annual deductions except for the first and last years.

Also, ABS must be used for any tax-exempt bond financed property. For example, governments that issue tax-exempt municipal bonds to finance property use the ABS depreciation method.

Cost basis details

Cost basis is a broad term that applies to many financial situations, but it’s usually known as the initial cost of acquiring an asset. This asset could be a property, equipment or an individual stock. If the asset’s market value exceeds the original cost basis, that person would have a gain. Conversely, if the market value is below cost basis, that would result in a loss. Cost basis also includes many factors like:

- Sales tax: The amount a business paid in sales tax when it purchased the asset. Consult this table for all current state tax rates.

- Shipping and delivery costs: Any shipping and delivery costs should be included in the cost basis.

- Installation charges: These charges relate to actions taken to place the asset in use. For example, the cost to hire an assembly line mechanic to set it up would be included in cost basis.

- Improvements: Improvements are a broad term that can be applied to a variety of assets. These improvements could be repairs or additional features that would make the asset more valuable. Improvements are especially important in rental real estate and IRS publication 527 goes into more detail on this topic.

Check out our guide to the Sales Tax for Small Businesses

MACRS depreciation method conventions

Conventions determine when the recovery life or useful begins and ends. It prorates the deduction businesses can take in the first and last years. The three types of conventions for the MACRS depreciation method are:

Mid-month

This method applies if a business places an asset in service or terminates it mid-month. It prorates the depreciation deduction by half a month, Keep in mind that this type only applies to residential and commercial property along with railroad grading/tunnel bore.

Mid-quarter

Mid-quarter convention as the name implies assumes installing or terminating the asset mid-quarter. Therefore, the deduction would only account for 1.5 months. It should only be implemented if mid-month isn’t applicable. Also, it would be applied if the total depreciable bases of installed or disposed MACRS property are more than 40% of the total depreciable bases of all MACRS property placed in service throughout the year.

It also doesn’t apply to residential, commercial property and railroad grading that has mid-month conventions. If this method nor the mid-month don’t apply, then businesses must use the half-year convention.

Half year

This convention can be used if mid-month or mid-quarter don’t apply. This will prorate deductions by 6-month increments and can apply to all types of property.

Specific recovery terms or useful life rules per asset

One of the main advantages that the MACRS depreciation method has over straight-line depreciation is that it has specific guidelines for each asset’s useful life. For example, residential real estate’s useful life is 27.5 years with commercial rental property having a useful life of 39 years. Here are some more specific examples per asset class:

- 3-year assets: Tractors and horses older than 2 years old.

- 5-year assets: Vehicles like cars, taxis, trucks, and buses. Office equipment like computers, machinery, copiers, R&D equipment and cattle. This also includes renewable energy and solar equipment.

- 7-year assets: Office furniture like desks, chairs, and file cabinets

- 10-year assets: Vessels, barges and agricultural structures. These include fruit-bearing plants.

- 15-year assets: Improvement to land, real estate or restaurants. Keep in mind that land isn’t depreciable as it will never break down. It’s also important to separate real property from improvements, especially during real estate sales.

- 27.5 year assets: Includes residential real estate placed in service after 1986. It’s further defined as a structure that derives 80% or more of the gross income from renting dwelling units. It doesn’t apply to dwellings that house transients like motels and inns.

Also, the recovery periods under the ADS system are generally longer. For instance, tractors that are rented to own have a period of 4 years, instead of 3. Any tree or fruit-bearing vine has a useful life of 20 years, which is double the useful life under the GDS. The reason for this is that GDS applies to more assets and is easier to use. ADS can be applied to fewer, more complex scenarios like real property outside the US along with tax-exempt property.

MACRS depreciation method calculators and resources

- Form 4652: This important IRS form allows business to calculate depreciation and it must be included in each person’s tax return. It’s a complex form for novices, which makes possibly consulting a qualified tax professional a smart move. It has many depreciation sections and areas for MACRS property, which enables businesses to not leave out important details. It’s also wise to be aware of the 50% business use section, which determines listed items. This, in turn, impacts bonus depreciation rules.

- Quickbooks: Quickbooks is an Intuit product and is a very helpful tool for small business. It can help self-employed people calculate and file estimated payments, provide financial statements and depreciation schedules. This software also has areas that help businesses record loan details and payments on depreciable assets. While Quickbooks doesn’t automatically calculate depreciation, businesses can manually track depreciation using journal entries. Assets that are being leased to own can be depreciated, but temporarily leased assets can’t be depreciated.

- Depreciation Calculator: The MACRS depreciation method is more complex than straight line and this calculator can help people accurately calculate it. It has many inputs for items like property types, section 179, business use percentage, listed assets, and business use percentage.

- IRS Pub 946: Businesses can use this resource that acts as a catch-all for every type of depreciation, specific rules and regulations. This publication provides detailed information on factors like inventory, time periods, special depreciation and business miles. As discussed earlier, it’s imperative to calculate business miles which can be done with the mileIQ app. This app segregates business miles and automatically calculates driving deductions.

- IRS Pub 527: This publication goes into detail regarding depreciating rental real estate. Rental real estate is an important asset class that has its own specific rules. This publication also sets guidelines for determining qualifying improvements, which impact cost basis. In turn, it also impacts recapture and sales proceeds.

- Sales tax rates by state: Sales tax adds to your cost basis, which impacts depreciation and lowers taxable gains. This table breaks down sales tax by item and rate per state.

MACRS and the solar industry

The Solar industry is very unique as it’s relatively new, growing rapidly and has many tax deductions like MACRS. Solar also offers businesses the investment tax credit (ITC), which allows businesses to deduct 30% of the installation cost from federal taxes. This tax applies to both residential and commercial systems of any value. The ITC was created in 2005 to support green policies and can be rolled over into future years.

The ITC is relevant for the MACRS depreciation method because it enables solar business owners to reduce the basis by 50% of the ITC. This results in a total basis of 85% which is calculated by 100 – (30% ITC x 50%). So, a solar panel worth $100,000 would have a basis of $85,000 and solar panels fall under the 5-year rule, which is the general payback period for solar investments in states like Oregon. The certainty of the MACRS depreciation method has also motivated high investments in solar and related energy projects. It also enables businesses to see a quicker return on investment (ROI) than other projects like commercial real estate.

Another factor that has prompted solar’s growth has been the reduction of corporate taxes to 21%. Prior to the Trump administration, the US had the highest corporate tax in the world at 35%. Lower taxes and more tax deductions have increased growth for all industries, not just solar. These policies have been proven to be a triple win scenario for businesses, the government, and the environment.

Bottom line

The MACRS depreciation method can be complex, but it’s an important tool that businesses use to reduce tax liability. Depreciation also impacts other financial statements like the income statement and all businesses use it. Thus, it makes sense to learn the fundamentals and how to use a standard MACRS calculator along with general laws. Small businesses don’t need to become the expert on every single MACRS method depreciation rule, just the ones that apply to their needs. Some main points to remember about the MACRS depreciation method include its formula, asset classes, resources, and real-world application.