Luckily, small business and self-employed people are entitled to many tax deductions and credits. These items allow them to lower their taxable income and pay fewer taxes. There are numerous methods to do this, with depreciation being one of the more important deductions. Simply put, depreciation accounts for an asset’s loss of value of time. Many assets like real property, vehicles, software, and office equipment are depreciable.

However, small businesses should know that land never depreciates as it can never become obsolete. This guide will teach small businesses about straight line depreciation in great detail and will include relevant resources, case studies, along with information on related topics.

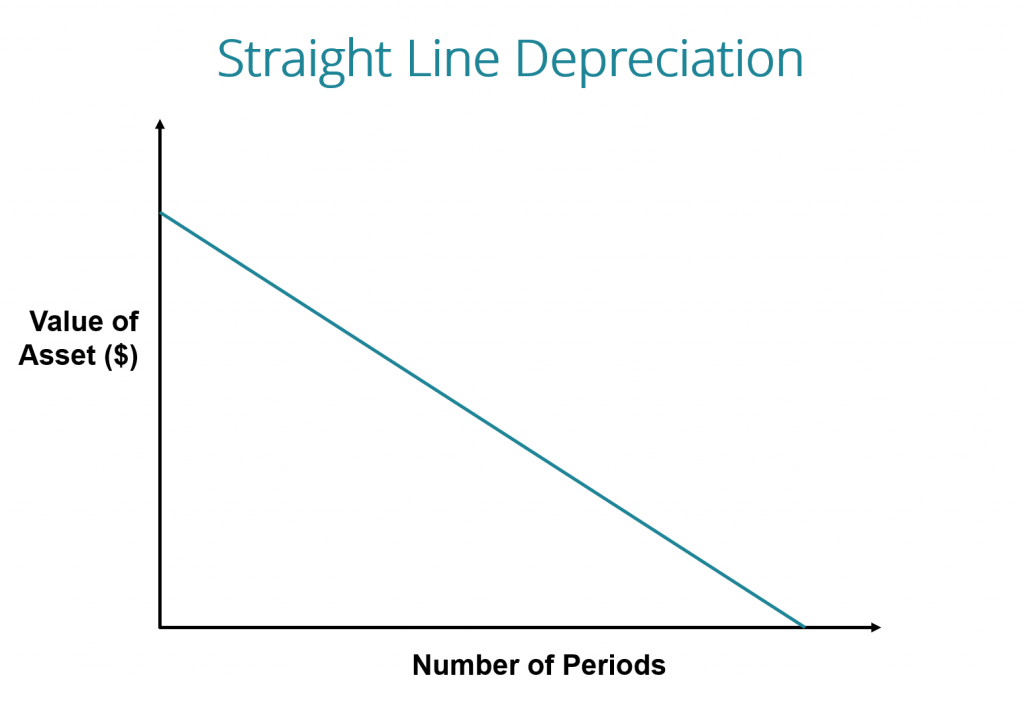

What is straight line depreciation and how does it work?

Depreciation is used for both accounting and tax purposes. For example, businesses include depreciation in their accounting processes by factoring the item’s decrease in value over its useful life. Depreciation is included as a line item towards the bottom of the income statement. It impacts net income by lowering the EBITDA or the earnings before interest, taxes, depreciation, and amortization. The main tax goals of using depreciation include staying compliant with the IRS and lowering taxable income. Each asset must follow specific rules in order to be depreciable like:

- Being held for at least a year

- The asset must be owned by the business. So temporarily leased assets can’t be depreciated.

- It has to be used in the business or any income generating activity. Items that are used for decoration purposes can’t be depreciated.

- It needs to have a specific useful life. The useful life is the time period in which the asset can still provide value to the business prior to breaking down.

The main two types of depreciation are straight-line and modified accelerated cost recovery system or MACRS. The straight line method is simpler and it allows businesses to deduct the same annual depreciation deduction over an asset’s useful life. For example, a business has a piece of equipment worth $60,000 that it can depreciate in equal annual installments of $5,000 over 10 years. This annual depreciation amount doesn’t change, which is why straight-line depreciation is fairly simple.

Conversely, MACRS allows businesses to have higher depreciation deductions in earlier years that gradually decline over time. MACRS also has stricter rules regarding specific assets, which include having specific useful life terms. For instance, the useful life of residential rental property is 27.5 years with commercial rental property having a useful life of 39 years. In fact, real estate that is put in place after 1986 MUST use MACRS.

Depreciation and amortization are similar as they both refer to an asset’s decline in value. However, depreciation applies to tangible assets while amortization applies to non-tangible assets. Some non-tangible assets include trademarks, patents, goodwill and various types of loans. One common example of amortization includes using a mortgage amortization calculator, which shows borrowers how much they will pay in principal and interest over its term. It’s important to note that businesses can only use the straight line method of depreciation regarding intangible assets. This reason for this is that intangible assets are harder to value than tangible ones.

Another type of depreciation is called depletion, which reflects the costs of extracting natural minerals like oil and timber. Oil and Gas companies commonly use depletion as oil extraction contributes to a large portion of their revenues.

Don’t have a business yet? Consider starting in Michigan, forming your new business in Indiana, or starting that new venture in North Carolina

Check out our guides on EBITDA and MACRS

Straight line depreciation formula

The main formula for straight-line depreciation is simply: The purchase price of an asset less salvage value/useful life. This formula will allow each business to know what it can deduct per year over the asset’s useful life. For example, a company buys an assembly line for $60,000 that has a salvage value of $10,000 and a useful life of 10. Thus, the annual depreciation expense would be $5,000.

The salvage value represents the total proceeds a company could receive by selling the asset at the end of its useful life. Salvage value is also referred to as residual value and some businesses can struggle with calculating an accurate figure. In this case, it could simply divide the purchase price/useful life to find the annual depreciation deduction. So the same company above would report an annual depreciation expense of $6,000. However, businesses that use this simplified approach need to record gains from the sale of the asset, which would be taxable.

Section 179 and bonus depreciation

Another important concept related to depreciation is Section 179 expensing. This rule allows businesses to deduct the entire cost of a recently purchased asset up to $1,000,000. Section 179 allows the business to accelerate depreciation into the current year and can be a valuable tool. However, there are some rules that each business should know:

- Section 179 deductions phase out once the total cost of the property exceeds $2.5 million. This is known as the investment limit and was formally $2.03 million in the tax year 2017.

- The Section 179 expense deduction is split evenly between spouses. So if a business owner files a married filing a joint or separate tax return, it will be split 50-50 between spouses.

To learn more about these specific rules, consult IRS publication 946.

Section 179 might seem complex, but this example will simply it. This picture assumes an asset purchase of $1,150,000 and a tax rate of 35%.

Bonus depreciation is another important concept related to Section 179 and it allows businesses to deduct 100% of the remaining basis. So, in this example, $150,000 is the remaining purchase price or basis after the 179 exclusion. Therefore, a business could deduct this entire amount in the first year thanks to bonus depreciation rules. Like section 179, bonus depreciation only applies to listed property, which refers to property that has at least a 50% business use. Some common examples of listed properties include computers, software, equipment and automobiles weighing less than 6,000 pounds.

Depreciation calculators and resources

Form 4652

Businesses use this form to calculate depreciation and include it with their tax returns. This form can be tricky to fill out at first, which is why it would be prudent to work with a qualified tax professional. It’s also all-encompassing as it has sections for straight-line depreciation, amortization, listed assets, time frame assets, and MACRS. It helps business ensure to account for all items and not leave out important details. One important section to pay close attention is the 50% business use section. Businesses can list items that are used for more or less than 50% for business use, which impacts bonus depreciation rules.

Amortization Calculators

As mentioned earlier, amortization is just depreciating non-tangible items. The most common example is a mortgage or loan amortization schedule which can be found in the here. This resource allows people to calculate amortization for a variety of loans and will show the monthly payment, total interest paid and suggests loan options.

Depreciation Calculator

Since straight-line depreciation is somewhat simple, most people can just calculate it with a standard calculator. However, this detailed depreciation calculator is very useful, when calculating MACRS depreciation. It has fields that account for the type of property, date placed into service, 179 deductions, listed assets, business use percentage and more.

IRS Pub 946

This IRS publication educates businesses on the types of depreciation, specific rules and regulations. This form goes into detail on a variety of concepts like home offices, inventory and specific time periods.

Form 4797

This form is used to record the sale of business property. It’s an all-encompassing form that has areas for section 1245, 1250 and other types of property. It can be used by a variety of persons including sole proprietors, contractors, S corps and partnerships.

Pros and cons of straight line depreciation

Straight line depreciation has its own unique pros and cons which include:

Pros

- Simplicity. Straight-line depreciation is easier to calculate than MACRS. Thus, it has less room for error and makes accounting/taxes more streamlined. Thus, this method is optimal for businesses that have simple equipment and operation types.

- Great for assets with relatively short useful lives. Straight line depreciation provides a higher deduction for businesses with useful lives of 10 years or less. It could make sense to use MACRS for assets with long useful lives.

Cons

- Can’t accelerate deductions into a shorter time frame.

- Useful life can be difficult to estimate. With MACRS, useful life is already determined for specific asset classes like residential and commercial rental property.

ACM depreciation case study

The fine details of depreciation can be quite complex, especially when it applies to decorations vs necessary structures of the building. One of the most important rules of determining a depreciable asset is if it’s used in income-producing activities.

One case study that proved decorations were actually necessary to the business and therefore depreciable was one company’s use of aluminum composite material or ACM panels on windows. These panels are used by a variety of industries like auto manufacturers and construction. ACM panels might seem like decorations, but they provided insulation and window support. Without them, water and other debris could easily enter the building.

A key takeaway from this example is to be aware of each item’s purpose. Some items like ACM panels might seem like decorations but provide a more important purpose. Thus, they would be depreciable and other team members like architects along with other design professionals should be aware of these basic tax rules.

Straight line depreciation and asset sales

Depreciation can become more complex, especially when it comes to asset sales. One concept to pay attention to is called recapture, which results in paying extra taxes when an asset is sold. Recapture is basically the government’s way of recovering any lost tax breaks due to depreciation. This applies when an asset is sold for above its purchase price or cost basis.

Straight line depreciation allows owners to reduce the asset’s cost basis over time. Therefore, it’s more likely that the owner will have a taxable gain. Also, this gain would be taxed at ordinary income rates, not the more favorable capital gain rates. The reason for this is that depreciation expenses reduce ordinary income.

One asset that would receive partial capital gains rate treatment is real estate. Real estate has a hybrid of tax treatments and is known as “unrecaptured section 1250 gain.” This rule also applies to other types of real estate including barns, commercial buildings, warehouses, and their structures. However, tangible personal properties and land don’t fall under this rule. For example, a printer inside an office building would be subject to section 1245 instead.

Section 1245 is a broad rule that captures all tangible and intangible property subject to depreciation or amortization. This also includes items that aren’t attached to the building. Conversely, a stove that is attached inside a building would be considered section 1250 property instead. Fortunately, most major tax forms regarding this concept have areas where taxpayers can segregate each asset type.

How to legally avoid recapture and taxes

One way to avoid taxes or depreciation recapture is through a 1031 exchange. Many real estate owners are surprised by recapture and high taxes due to profitable sales. A 1031 exchange would allow the owner to take the sales proceeds and invest it into a similar asset without paying taxes on the gain.

This is also known as a “like kind” exchange since the owner is exchanging a like kind asset for another. A 1031 exchange can be used to acquire rental properties and passive income via monthly rents. Also, this rule only applies to domestic US real estate. There are other variations of this rule like the 1035 exchange which allows people to sell and reinvest life insurance proceeds into another similar policy tax-free.

Bottom line

Depreciation is one of the most common and important ways to reduce taxable income. It also influences income statements and all businesses use depreciation in some form or another. Therefore, it’s important to know the basics of this concept, especially straight line depreciation. The fundamentals of straight line depreciation are relatively easy and most assets, excluding land, can be depreciated. Some main takeaways to remember about depreciation include its formula, methods, resources, forms and real-world application.